A Contractor's Guide to Functional Analysis

INTRODUCTION

Hard times teach hard lessons. The great recession of 2008 has alerted the construction industry to the fact that it cannot rely on boom times and unlimited growth to insure profitability. Shrinking revenues over the past six years have inspired contractors to take a closer look at their management practices and search for ways to maintain profitability in the absence of top line growth.

During the decade preceding the recession of 2008 SMACNA contactors built efficient and professional home office organizations. When the market turned down they were reluctant to dismantle these carefully erected organizations and began searching for top line growth wherever they could find it. They were trying to preserve their organization for the inevitable return of good times.

Unfortunately, all top line growth is not created equal. The contracts that many SMACNA contractors pursued were not profitable. They either traveled too far from their normal base of operations or took work that was outside their area of expertise. In most instances they supported their overhead organizations but eroded profitability.

We asked this question: Is there a way to manage overhead in lean years without dismantling an organization?

The answer: We must learn to look at things differently. We must learn to manage organizations more efficiently beyond simply "cutting overhead".

Why can't we view a company as an outcome produced by an arrangement of inputs?

By utilizing the principles of Functional Analysis, we were able to see clearly for the first time how a company actually accomplished its ends. We could see the sequence of activity and the building-block-nature of each function. Finally, we saw clearly for the first time exactly what outcome we were working for.

Functional analysis is a refreshing mental exercise that generates valuable insights beyond your expectations. It takes practice to get the most out of it. We recommend that you make it an essential part of your annual planning cycle.

Sheet Metal and Air Conditioning contractors like other construction contractors have traditionally developed their organizations on an as-need basis. When an owner can no longer do all the work himself, he hires someone to help out. As the workload increases that person hires someone to give him a hand and so on down the line. Sheet metal and A/C companies typically grow their organization when an increase in work demands an increase in workers. Nothing could be more natural. We describe this as organic growth.

As long as a spontaneously increasing workload compels the growth of the workforce, no one ever questions organizational growth. The workforce is always running to catch up with the volume of work and remains naturally efficient as a result. This kind of natural organic growth seems both logical and compelling and is rarely conceptualized after the fact.

THE PROBLEM

Sooner or later, the overhead organization outgrows the workload. Department heads have hired and trained a staff that they believe can handle the existing work efficiently. Each department becomes the fiefdom of the department head, and he fights to preserve his organization at all costs. Research shows that at this juncture in a company’s life cycle senior management’s initial response is to chase new business to cover the overhead already in place. Top line growth as a solution to shrinking profitability has become a reflexive response. Senior executives across all of American industry fall prey to this reflex. Top-heavy organizations seek new, often unprofitable, work to prop up their top-heavy organization. The need for ever increasing revenues to support existing overhead leads to poor pricing disciplines in the contracting business, that result in unprofitable contracts. Unprofitable contracts lead to an increased debt burden required to finance the bloated overhead, and profit is eroded further. Too often sustaining the overhead becomes the company’s mission, not profitability.

The top 25% of contractors surveyed by SMACNA in 2012 reported a 4.7% decrease in revenue per employee. However, the median SMACNA contractor, who did not grow as rapidly, reported an increase in revenue per employee of 3.1%.[i] As SMACNA companies grew bigger the revenue per employee actually decreased, a clear indicator that top line growth does not necessarily lead to increased profitability.

Overhead organizations initially grow in response to the demands of the workload, but once these organizations evolve into existence, executives are loath, or frequently unable, to “re-conceptualize” them. Rarely are overhead organizations designed specifically for the work that requires their existence. Therefore, the willingness and ability to “re-conceptualize” an organization chart is a critical step toward insuring the continued incremental growth of a contractor’s profitability.

TRADITIONAL ORGANIZATION CHART

The purpose of conducting a functional analysis is to create a dynamic, rather than a static view of an organization. In most companies the formal organizational structure is delineated by a chart (combined with additional verbal and written explanations). These representations usually focus on management levels, span of control issues, and who is responsible for decision making in each area of the business. Usually they identify the

specific personnel occupying the positions. This tells us what a position is but does not identify what it does. It offers no insight into what contribution each position makes to the ultimate corporate outcome. Traditional organization theory divides corporate organizations into departments and assumes that the title of the department implies what it does. The inputs (functions) that generate outputs leading to the ultimate corporate outcome are only implied but not identified or measured. When you look at your static organization chart no management action is suggested. It is simply a picture of your organization at one moment in time. The traditional organization chart is an inert management report.

Figure 1. Sample Sheet Metal and A/C Contractor

(Chart Graphic Here)

Organization Chart

Organization charts, like balance sheets, are snapshots in time. They offer a picture of the extent and structure of the current overhead organization. They are not management tools unless management can examine them with new eyes.

NEW EYES

Engineering theory utilizes a design approach called FUNCTIONAL ANALYSIS, described as the process of identifying design parameters that satisfy functional requirements.[i]

Functional Analysis, when applied to designing organizations, is the discipline that analyzes the activities an organization must perform to achieve its desired outputs.[ii]

To analyze the efficiency of an organization:

· Functional Analysis starts with an empty organization chart.

· Identifies the ultimate desired output of the firm.

· Identifies inputs essential to achieving each area’s output.

· Groups inputs into activity areas called functions.

· Charts work flow to reveal conflict and redundancy.

· Converts inputs to positions.

· Quantifies each position as an equivalent employee (EE).

· Assigns a cost to each equivalent employee (input).

· Calculates the cost of the resulting chart.

The resulting organization chart defines the manpower and financial budget required to achieve the desired output. By simply comparing the organization chart arrived at through a functional analysis with the existing organically grown organization, inefficiencies become immediately apparent. The functional analysis chart is the organization we should have to achieve our desired output. Our existing organization chart is simply the one we do have.

WHY FUNCTIONAL ANALYSIS

When conducting a functional analysis we view a corporate organization as a collection of inputs or “functions” that contribute to achieving the desired corporate outcome.

A function is defined as a series of related activities, involving one or more entities, performed for the direct, or indirect, purpose of fulfilling one or more missions or objectives of the firm, generating revenue for the firm, servicing the customers of the firm, producing the products and services of the firm, or managing, administering, monitoring, recording, or reporting on the activities, states, or conditions of the entities of the firm.[iii]

THE FUNCTIONAL ORGANIZATION CHART

A functional analysis creates a dynamic representation of what each position in the organization actually does to contribute to the corporation’s ultimate outcome. It traces the work flow from the initial project concept to the ultimate outcome and evaluates the efficiency and cost of each contributing function.

A contractor needs to coordinate a wide variety of functions to create a single ultimate outcome. A functional analysis depicts the flow of these essential functions (inputs) across the different activity areas that contribute to the ultimate corporate outcome. The resulting chart reveals inefficiencies, conflicts, blockades, and redundancies that have a negative effect on productivity and profitability.

STARTING AT THE END

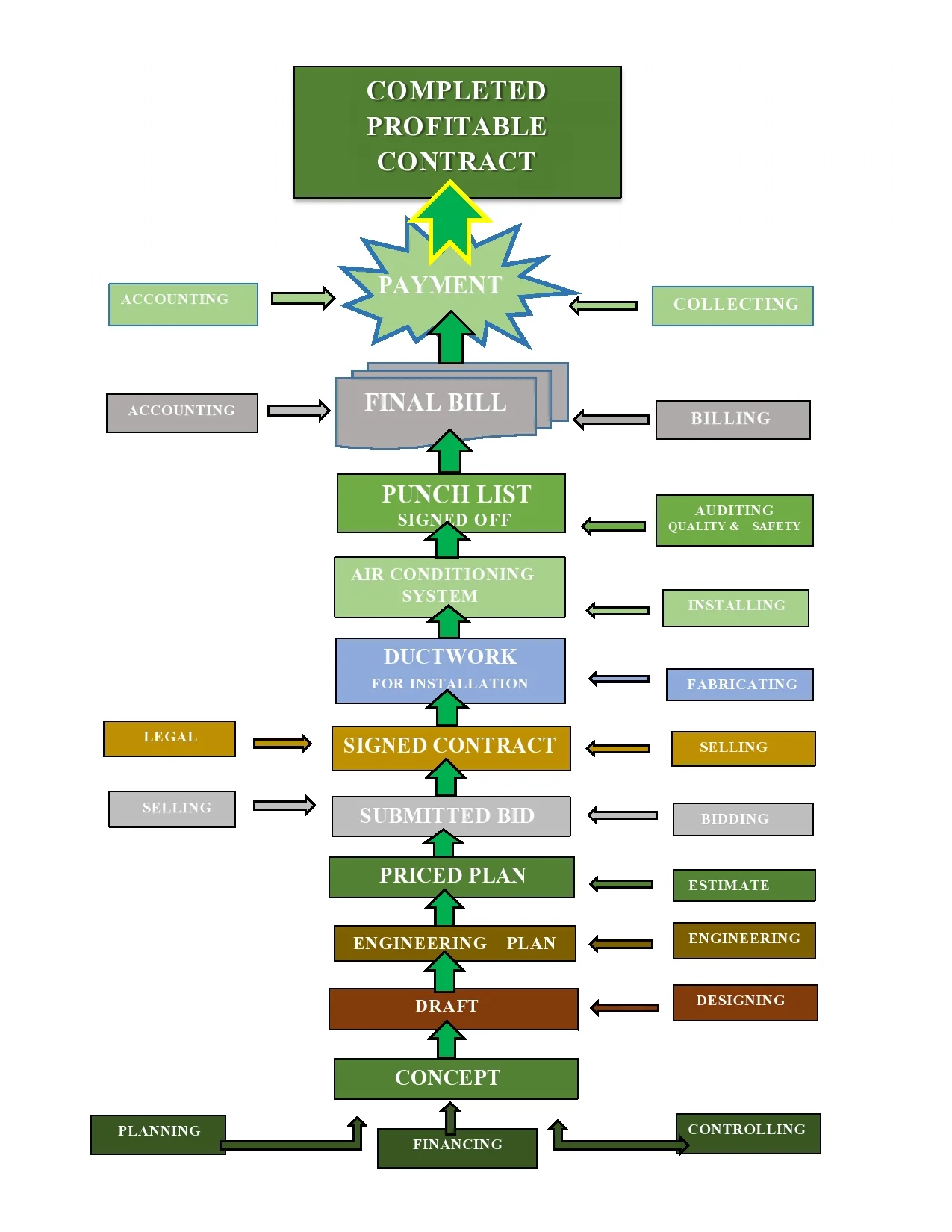

A functional analysis begins by identifying the ultimate outcome the company is trying to achieve. The ultimate outcome is not only “what” the company produces. It is also “why” the company produces the “what”.

Figure 2 is a dynamic representation of sequential inputs combining to create an ultimate corporate outcome. Each input or function is required at a specific stage of development, and every input builds on those that came before. The impulse to seek any contract is initiated by the owner or CEO, financed by his office, and pushed into the first stage of the corporate pipeline. The functions (inputs) of creating, planning, financing, and controlling are all initiated by the owner or CEO’s office. The concept then moves through design and drafting to engineering and estimating before it can be priced for bidding and ultimately executed in the form of a contract bid. The sales department then joins with the legal department to turn the contract bid into a signed contract. A signed contract is nothing more than an authorization for fabricating, engineering, and installation to begin to add their inputs. Accounting begins to add its input by tracking expenses to measure if this contract will ultimately become a profitable contract. The fabricators add their input, along with the project managers and on-sight supervision, to ensure that the final element of "COMPLETED" will be added to "PROFITABLE" and "CONTRACT", to finally produce the ultimate corporate outcome.

Figure 2. Typical Sheet Metal and A/C Contractor

Functional Analysis Chart

STEP ONE: IDENTIFYING THE ULTIMATE OUTCOME

If you don’t know where you’re going, you’re probably not going to get there. ~ Ancient Chinese Proverb

ONE FOR ALL - ALL FOR ONE

All SMACNA contractors are single purpose organizations. The fabricators, however, probably believe that they produce a distinct product, (ductwork, architectural metal, roofing, etc.) that is sold to the client. The installers believe they provide a service (installed air conditioning or other systems) to the customer. Purchasing believes that when they deliver materials and equipment to the fabricators and installers, their job is done. The accountants see their product as accurate and current financial statements, and their customer is senior management. Once they deliver accurate reports when requested, their job is done. The lawyers work for the CEO to keep the company within specified legal boundaries. Everyone believes that they have a distinct product and customer.

This diversified view of products and clients held by most employees is common across all industries. A fragmented corporate self-image can lead to inter office politics, competitive conflicts, duplication of effort, and self-protective behavior that damages the efficiency of the organization and the quality of its intended outcome.

THE ULTIMATE OUTCOME

The first step in a Functional Analysis is to identify the sole corporate purpose to which every position, function, activity, and input is dedicated. This is called the Ultimate Outcome. Identifying your company’s ultimate outcome requires thinking beyond product to purpose. It requires seeing the why of a corporation beyond its how.

While preparing this paper, we conducted an anecdotal survey of stake holders in the Sheet Metal and Air Conditioning contracting industry. We asked one simple question without preamble or explanation: What is the purpose of your company? We received the following replies:

1. “To deliver Cool Air to the customer”

2. “To install Air Conditioning equipment”

3. “To manufacture and install high quality air handling equipment”

4. “To fabricate and install architectural metal.”

5. “To fabricate and install metal roofing systems.”

All participants correctly identified the products they sell. They did not identify their Ultimate Corporate Outcome.

The obvious purpose of a construction contractor is to contract to do something. If that were all, the contractor would need only a salesman and a lawyer, and he would be in business. However, the contract calls for a job-of-work that the contractor must perform. In other words, they must complete the contract. When they do, they will have satisfied the customer’s purpose for entering into the contract. They have not, however, satisfied their purpose for entering into the contract. They want to make a living. They intend to have some money left over after paying all the expenses required to complete the contract. Their purpose is to make a profit.

The ultimate desired outcome for all contractors, therefore, is:

COMPLETED PROFITABLE CONTRACTS

STEP TWO: FUNCTIONS

After identifying the ultimate desired outcome of a company, a functional analysis goes on to identify the functions, or the well thought out collection of inputs, that produces, in the SMACNA contractor's case, a COMPLETED PROFITABLE CONTRACT.

Traditionally, contractors view their overhead organizations through the use of charts that identify positions, reporting lines, and department groupings, but only imply what input each position contributes to the department’s output. It is the functions that each position performs that functional analysis is concerned with.

WHAT IS A FUNCTION?

Functions are defined as collections of inputs necessary to create desired outcomes.

Inputs are divided into collective activity areas that produce outputs. Each of these “activity areas”, made up of a collection of diverse inputs, is called a function. When combined with other functions they collectively produce the ultimate corporate outcome.

A typical SMACNA contractor, for example, may need the input of the engineering and design office, the estimating office, the purchasing department, the fabrication shop, the project management office, the accounting department, and the legal department to produce a COMPLETED PROFITABLE CONTRACT.

ESSENTIAL SMACNA FUNCTIONS:

C.E.O. - (Planning/Financing/Controlling/Hiring/Training)

Designing - (Drafting)

Engineering - (Drafting) (CAD)

Estimating - (Purchasing-Accounting)

Bidding - (Estimating-Selling)

Selling - (Estimating-Bidding)

Contracting - (Legal-Selling)

Purchasing - (Accounting)

Accounting - (Auditing)

Fabricating - (Supervision)

Installing - (Controlling)

Auditing - (Safety/Quality/Cost)

Billing - (Accounting)

Collecting - (Accounting)

STEP THREE: FIRST DAY IN BUSINESS ANALYSIS

When functional analysis planners analyze each contract they look at the company overhead as if it wasn’t there. They begin only with the contract and decide which functions are required to sign the contract, complete the contract, and see that the contract supplies the company with a profit. Making a simple list of the inputs required starts the planning process. Next, they assign the inputs to functional areas and plot the flow of work from the early inputs through the interim steps and out to the final outcome. Their experience will enable them to assign a cost factor to the inputs, and the result is an efficient chart of the work flow it will take to achieve the desired corporate outcome.

The purity of the thought process is what makes it so valuable. No personal considerations, emotional influences, traditional imperatives, or hubris is involved. Thinking only of the inputs it will take to achieve desired outputs casts a whole new light on organizational design.

Because it is impersonal and seems to put all positions at risk, this discipline has not achieved popularity. However, the “First Day in Business” approach is a must. It doesn’t reflect on existing people, or history, or tradition. It starts from scratch. It’s the zero-based-budgeting of personnel management.

STEP FOUR: A FUNCTIONAL ORGANIZATION CHART

Charting an organization by function rather than position offers a dynamic view of how a contracting company achieves its ultimate outcome. The essential inputs we identified in Step Two function in activity groups for control and cohesion. By turning the ultimate corporate outcome back into functions we can see how the inputs interact and flow toward the outcome. The resulting chart can reveal redundancy, improper coordination of effort, conflicts of purpose, choke points, and inefficiencies that are easily corrected when finally noticed. A traditional organization chart tells none of this story.

PRIMARY FUNCTIONS

In my book, Construction Contractor's Survival Guide, I identified the three primary functions of the construction business as: (1) Getting the Work, (2) Doing the Work, and (3) Accounting for the Work.[i] A functional organization chart begins with the ultimate outcome at the very top of the chart’s hierarchy.

COMPLETED PROFITABLE CONTRACTS

These are the essential elements of our ultimate outcome. The next question is, which inputs contribute to our three primary functions?

DOING THE WORK

ACCOUNTING FOR THE WORK

GETTING THE WORK

This is the beginning of a functional analysis. By listing inputs essential to SMACNA contractors under the appropriate primary function, you will begin to develop a picture of how the work of a SMACNA contractor should be organized. Then you will be able to chart the flow of work from one activity area to another, testing synergies, efficiencies, redundancies, and conflicts enabling you to design efficient work flow contract by contract.

STEP FIVE: THE SMACNA FUNCTIONAL CHART

A functional analysis deals with the inputs of each function. It is designed to chart input activity, not positions or responsibility. A functional analysis is trying to identify the work inputs that create the outcomes. It is intended to show how the work of one function builds on the work of another until the goal is reached.

For example, the Project Manager may not think the Accounting Department is there to help him. He believes they are there to point up his mistakes and report them to upper management. If, however, he understands that the Accounting Department is there to quantify the work in progress and alert him to waste, he accepts how the contribution of each input or function supports the contribution of the other. Everyone is responsible for the entire ultimate outcome. Functions differ, but the outcome unifies all inputs. Introducing these concepts throughout the organization has huge benefits. The Project Manager, for example, is responsible to see not only that the work gets done but to see that the work is profitable. He not only insures that the contract is completed, but that it is a Completed Profitable Contract.

EXCERPT FROM WHITEPAPER.........